Form 1040 is the form individual taxpayers use in order to file their tax returns. You can find a ton of information on the 1040, today we will focus on the Income aspect.

Different aspects of your finances are collated via different other Forms and Schedules. All this information comes together in Form 1040 to determine your taxable income for the year, and therefore your tax liability for the year. It is the “final common pathway”.

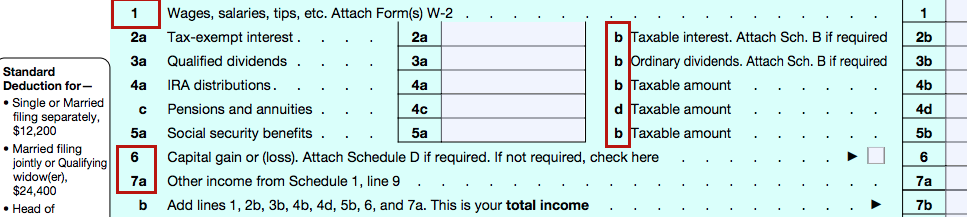

Total Income

This is line 7b of the new Form 1040. Form 1040 got a makeover in 2018, when the Tax Cuts and Jobs Act was passed. It is now simpler and sleeker. Or so Congress thinks.

You get to Total Income by adding the components on lines 1, 2b, 3b, 4b, 4d, 5b, 6 and 7a.

Line 1: Employment Income

Line 1 is the salary, as reported on your W2.

So, if you are an employed physician and are paid on W2 or owner-employee of an S-corp and pay yourself a salary, this is where it goes.

Line 7a: Other Income

All income that cannot be entered directly on Form 1040 (W2 income) goes on Schedule 1. For example, if you are self-employed.

Part I of Schedule 1 deals with Additional Income:

- Line 3 of Schedule 1 is where you enter your business income (or loss). This includes any 1099 income as an independent contractor or your net income as a sole proprietor. You also file a Schedule C to fully report your business income and expenses.

- Line 5 of Schedule 1 is where your partnership or S-corp distributions go. Plus rental real estate, if you have any.

- Line 7 has room for unemployment compensation. I’m including this here since 2020 saw some of us in those dire straits.

Add it all up on line 9 of Schedule 1 and that number then feeds into line 7a of Form 1040.

Line 2: Interest Income

- Line 2 is Interest paid to you.

- 2a is Tax-exempt interest, for example, income from Municipal bonds (these are federal tax-free, but may be taxed by the state).

- 2b is Taxable interest. This includes income from non-Muni bonds, bank accounts, etc.

- Interest income is reported to you on 1099-INT by each financial institution where you earned said interest.

- You also have to fill out and attach Schedule B if your total taxable interest income is greater than $1500. The total from line 4 of Schedule B feeds into line 2b of Form 1040.

Line 3: Dividend Income

- Dividend income goes on Line 3 of Form 1040.

- 3a is Qualified Dividends- which are taxed at the more favorable capital gains rates.

- 3b is Total Dividends, which includes Qualified and Ordinary Dividends. (Form 1040 calls 3b as Ordinary Dividends- making it confusing).

- Your dividend income gets reported to you on a 1099-DIV, one from every institution where the relevant accounts are held.

- Even if a mutual fund distributes Qualified Dividends, your dividends will be considered non-qualified if you did not hold the fund for more than 61 days of the 121-day period around the ex-dividend date. If your Total Dividends are greater than $1500 for the year, you have to file Schedule B.

Line 4: IRA Distributions

- Line 4 is next.

- 4a includes all distributions from IRA; 4b is only the taxable component of those distributions. Only 4b will feed into the Total Income.

- You receive a 1099-R for any IRA distributions you’ve taken.

- When you are a retiree and taking money out of your tax-deferred Traditional IRA to meet your spending needs, most or all of it will be taxable now at withdrawal.

- The rest of us should not be withdrawing at all from an IRA. But, you may still see a number on 4a. Either approximately $6000 or $12000, depending on whether you’re filing singly or jointly with spouse. That is, if you are doing the Backdoor Roth IRA every year.

- The conversion from Traditional IRA to Roth IRA, which is the basic premise of the Backdoor Roth, is counted as a distribution. But, fear not, this number doesn’t get added to your total income.

- 4b is taxable amount of IRA distributions. For those doing the Backdoor Roth, this may be zero or a tiny amount- a few cents to a few dollars.

- It comes from the small gain your Traditional IRA may have before you convert it to Roth. If the market rose in the couple of days before you made the conversion (as it does 77% of the time), that amount is taxable.

- Lines 4c and 4d refer to pensions and annuities and their taxable amount, respectively. This includes distributions from 401(k), 403(b), and governmental 457(b) plans.

- Rollovers from one qualified employer plan to another also go on lines 4c and 4d, depending on your cost basis in those plans.

Line 5: Social Security Benefits

- 5a is all Social Security benefits the filer received; 5b is the part on which taxes are due.

- You receive a SSA-1099 if you receive Social Security benefits.

- The proportion of Social Security benefits that is taxable depends on your “Combined Income”.

- “Combined Income”= Adjusted Gross Income + Nontaxable interest + 1/2 of your Social Security benefits

- The income limits are really low- for those married filing jointly, an income more than $44,000, in 2020, implies 85% of your Social Security income will be taxed.

- Ever wonder why there’s a tax on a tax? Here’s some history behind it.

Line 6: Capital Gain or Loss

- Investment income, ie., capital gains go on line 6.

- Long-term capital gains, on assets held for longer than a year, are taxed at a preferentially lower rate than ordinary income.

- Short-term capital gains, on assets held under a year, are taxed at ordinary income tax rates.

- You receive a 1099-B from the financial institution where the investment transactions happened. for example, if you sold any stocks or funds and made a profit. Or you tax loss harvested and had a “paper loss”- it’s all there on the 1099-B you receive from the brokerage house.

- Form 8949 and Schedule D are where the math is done and then fed into line 6 of Form 1040.

Line 7b: Total Income

Add all the above (lines 1, 2b, 3b, 4b, 4d, 5b, 6, and 7a) and you get Total Income.

This Total Income is then modified, in other words, “adjusted”, to arrive at “Adjusted Gross Income”. Stay tuned for that and more in next week’s post.

Questions or comments? Pen them below.