The market volatility due to Coronavirus fears presented a good opportunity to tax loss harvest (referred to as TLH hereon) in the beginning of March, 2020. There are some good blog posts about tax loss harvesting out there. Here, I wanted to lay out the steps for TLH’ing when you have ETFs rather than Mutual Funds of the Index Funds you invest in. Though the basic premise and reasons for doing so remain the same, some of the steps look a little different.

Why Tax Loss Harvest?

When there is a fall in market prices for any reason, the funds in your taxable brokerage account register a loss. Now, this loss is only on paper (or “unrealized”)- unless you sell low and “realize” the loss. Savvy investors that you are, you will not do that. You know to ride it out. However, there is one scenario where it may be of benefit to sell low. And that’s where TLH comes in.

By selling lower than you bought a fund at, you incur a capital loss. This lowers your next tax bill in one/both of two ways:

- it negates any capital gains you may have that tax period, say from selling investments that have had a gain or from real estate sale.

- If you have no capital gains to offset, you can offset some of your ordinary income. At your marginal tax rate. Which is why its capped at $3000 of ordinary income. If your loss is greater than $3000, you carry-over the loss into subsequent years, without any expiration date, $3000 at a time.

But selling at a loss, just to lower a tax bill is no winning strategy. You still took a hit and lost money. You just shared some of your losses with the IRS.

Unless you tax loss harvest it.

What is Tax Loss Harvesting?

If you buy back (at the low price) what you just sold at a loss- then you wouldn’t technically be losing any money. Even though you registered a paper loss and were able to lower your tax bill. Sounds too good to be true? Well, it isnt (almost- there’s always a catch, isn’t it?). It’s the miracle of tax loss harvesting.

BUT- there are do’s and dont’s from the IRS:

The “Substantially Identical” Rule

If you want to get back into the same fund, you have to wait at least 30 days. Most of us do not want to do that since the market may go up significantly in that interval. We want to sell and buy back right away.

In that case, you cannot buy back a “substantially identical” fund. The IRS does not delve deeper into this.

- It certainly means you cannot buy back the same fund. Even in the form of re-invested dividends.

- Or switch from Mutual fund format to its corresponding ETF, or vice versa.

- Whether a different fund that tracks the same index is substantially different is open to interpretation. However, there are enough choices among the broad asset classes of Index Funds, that you will find other Funds or ETFs to get into, to avoid the “substantially identical” conundrum.

For example, you sell Vanguard’s Total Stock Market ETF (VTI) and then go back and buy yourself some more VTI immediately. Not kosher.

But you could buy some VOO (Vanguard’s S&P 500 ETF). VTI and VOO have a more than 99% correlation since the S&P 500 (500 of the large-cap companies in the U.S.) makes up 80% of the U.S. Total Stock Market in terms of market cap.

In other words, over time, your investments would look remarkably similar whether you were in VTI or VOO.

Or you sell off VTI and buy Fidelity’s Total Market Index Fund (VSKAX). Fidelity’s Fund tracks the Dow Jones U.S. Total Stock Market. So, a different index from what Vanguard’s VTI does (CRSP Total Stock Market Index). But Total U.S. Stock Market exposure, nonetheless.

Similarly for Total International Stock Market. Some similar but not identical funds that do the trick are Vanguard Total International Stock Market ETF (VXUS), Vanguard FTSE All-World Ex-US ETF (VEU) or iShares Core MSCI Total International Stock ETF (IXUS).

So, what does happen if you use the same or a “substantially identical” fund? You don’t get the tax benefit of the TLH.

And that is called a Wash Sale.

Wash Sale Rule

IRS regulations state that if you sell a security at a loss and buy the the same or a substantially identical fund within 30 days before or after the sale, you are not eligible for the tax write off for the loss. Practically, all this means is:

- Make sure Dividend Reinvestment is turned off.

- If you are selling a fund in order to tax loss harvest, sell all the lots of that fund bought within the prior 30 days.

- If you want to get back into the same fund, wait at least 30 days.

- If you want to take advantage of market downturn, look for a TLH partner that is not substantially identical.

- If you do mess up any of these rules, you lose the tax benefit from the TLH.

Steps in Tax Loss Harvesting

I have my taxable brokerage account at Vanguard. And I am an ETFs (Exchange Traded Funds) gal. This is because I started my investing career with individual stocks- back before I had heard of Vanguard or Index Funds. Or the Roth IRA. So I just feel more comfortable with ETFs. They trade like stocks. Fortunately, they are also a hair more tax-efficient than their corresponding Mutual Fund version- though at Vanguard, this difference does not exist.

So, the skinny I’m laying here pertains to Vanguard ETFs. The example I am using is VIOV: Vanguard S&P Small-Cap 600 Value ETF. This is part of my small-cap value allocation in my portfolio. It is not my default small-cap value option. I got to holding it because of a prior TLH.

I made a mental checklist of the Do’s and Dont’s:

- I had held the ETF for more than 30 days

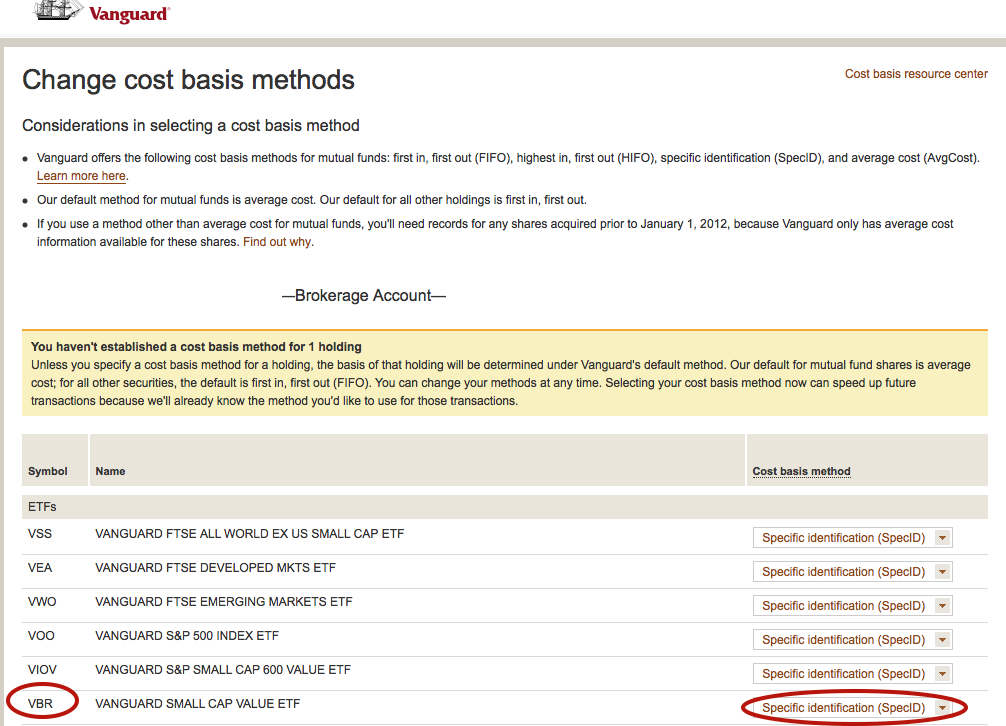

- My cost basis was set to Spec ID

- Automatic dividend reinvestment was turned off in my account

- It had just registered a significant loss (more than $5000)

- I didn’t want to wait for another 30 days to buy. So, I was not going to buy back VIOV or another small-cap ETF that tracks the S&P Small-Cap 600 Index. I was going back to my default option: Vanguard Small-Cap Value ETF (VBR). VBR tracks the CRSP U.S. Small-Cap Value Index and is arguably not substantially identical to VIOV.

The Steps to Tax Loss Harvesting at Vanguard with ETFs

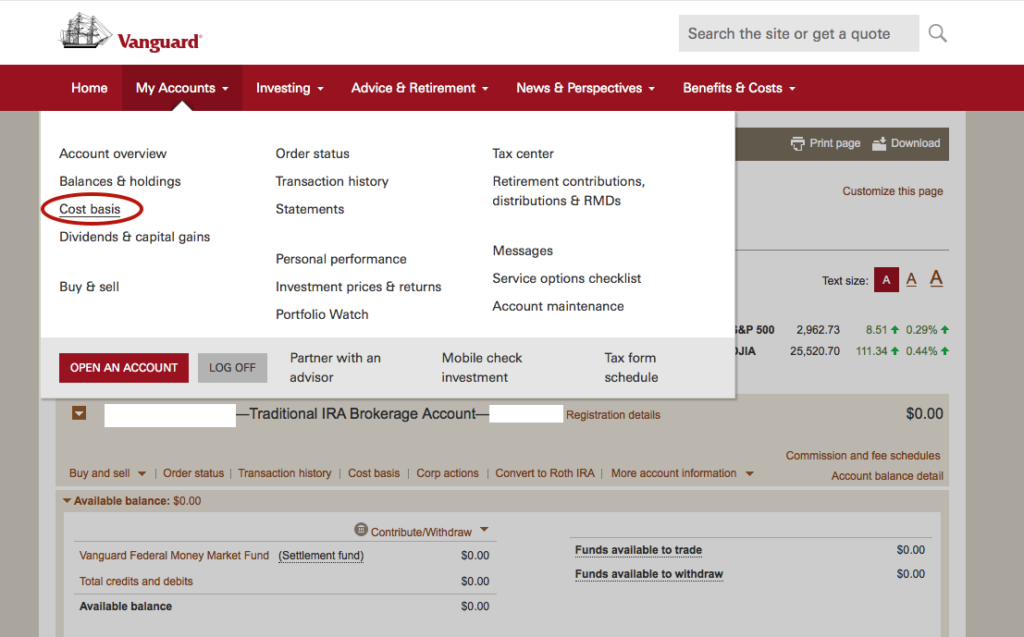

Login to your account at Vanguard. From the My Accounts tab, click on Cost Basis.

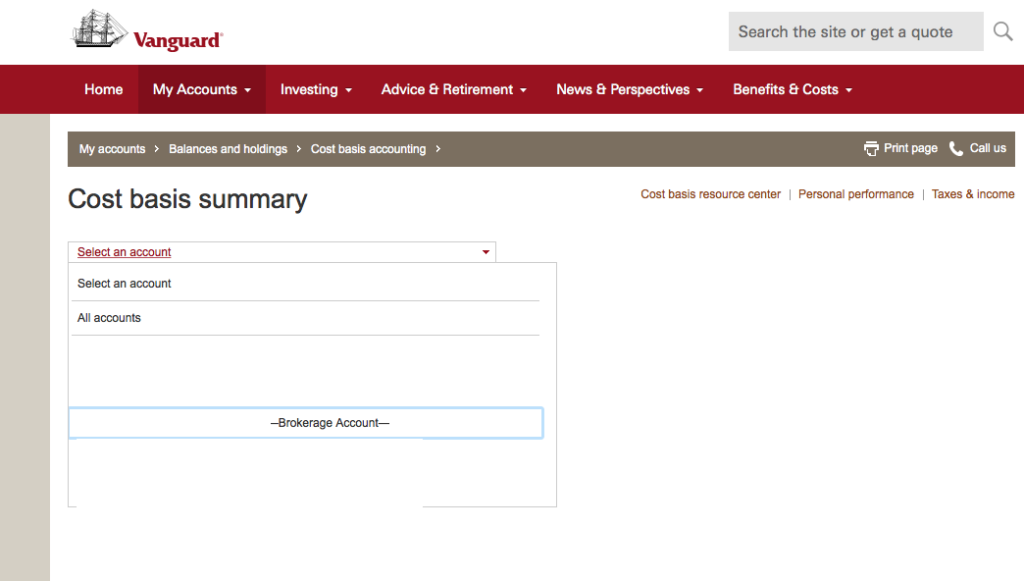

It will take you to the Cost Basis Summary page where it lists all of your accounts. You want to pick your taxable or Brokerage Account.

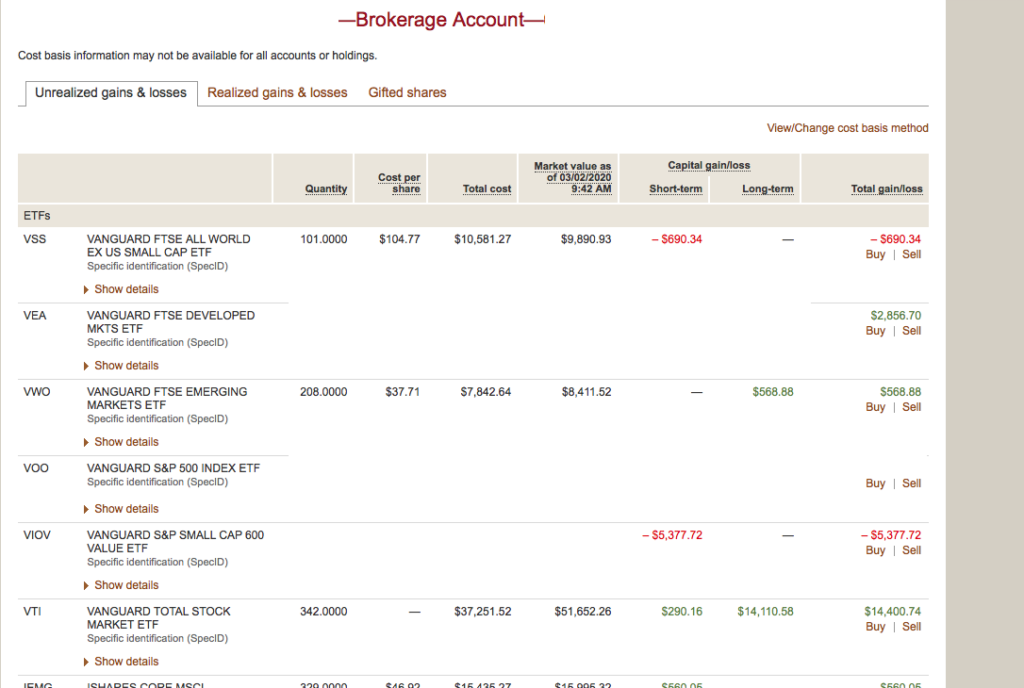

The Brokerage account’s Cost Basis Screen looks like this:

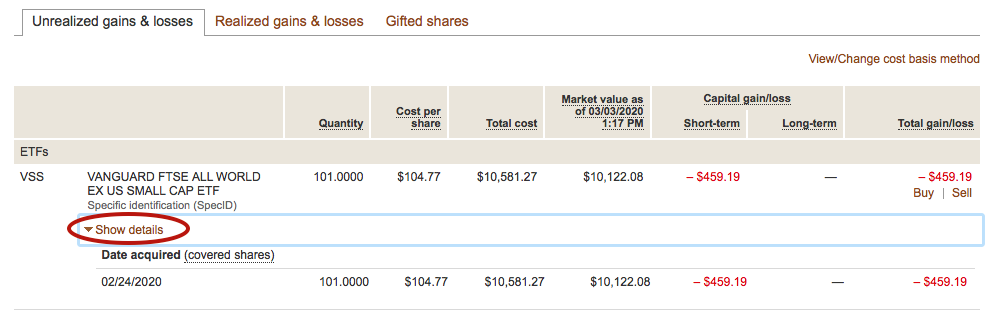

Please note, we are viewing the “Unrealized Gains & Losses”. Not a bloodbath here but enough for my purposes. Two of my ETFs have losses in them: VSS- an International Small-Cap ETF and VIOV- the U.S. Small-Cap ETF.

I will hold off on TLH’ing VSS since the loss is small and go only for VIOV today.

This is completely arbitrary. I used to have a smaller cut-off, about $500 to take the trouble to TLH. Now I let it slide if it’s less than $1000. There are no hard and fast rules about this. When your accounts are small, the losses will be smaller, too. Get your feet wet with small losses and you will be a TLH-pro by the time the numbers balloon. And you will be there, sooner than you think.

I do want to use the VSS to make a point since I don’t have that picture for VIOV. When you click on “Show Details” under an ETF, it shows you all the lots of that ETF you own, if you have set “Spec ID” as your default option. We’ll come to that later. Use this:

- to sell only the lots that have incurred losses.

- And to sell anything purchased within the prior 30 days

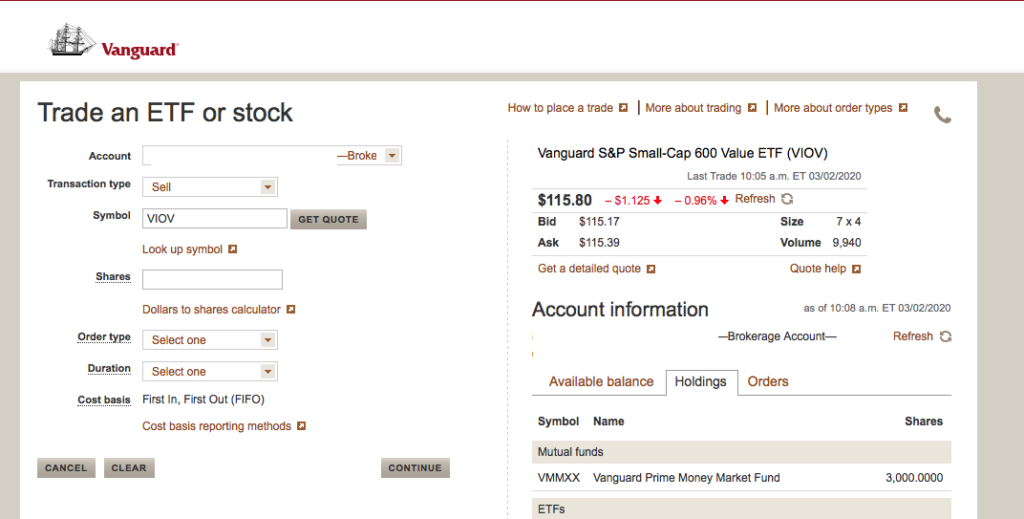

Sell VIOV by clicking the Sell in the rightmost column. Please note, there is no option for “Exchange” as you would typically see with Mutual Funds. With the ETF, I can see the exact price I’m selling at.

It takes you to this screen:

I wanted to sell all my VIOV: I had only 1 lot of it and hence, all of it had a loss. Use the second (Quantity) column to see how many shares you’re selling:

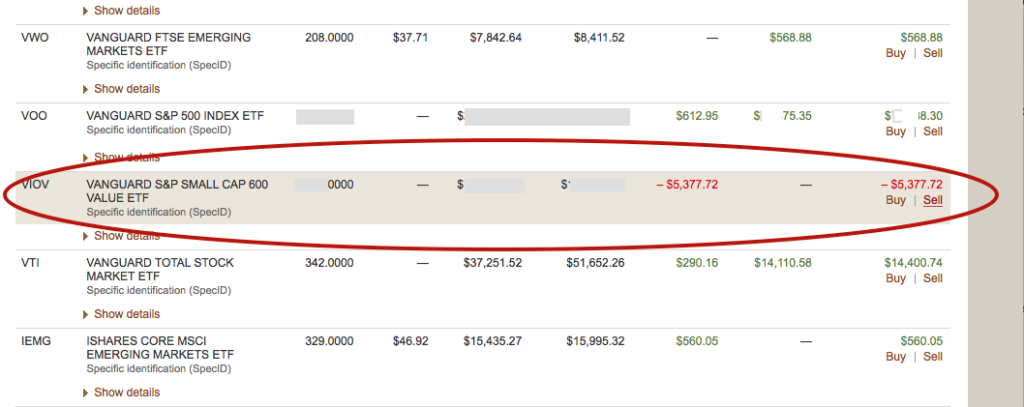

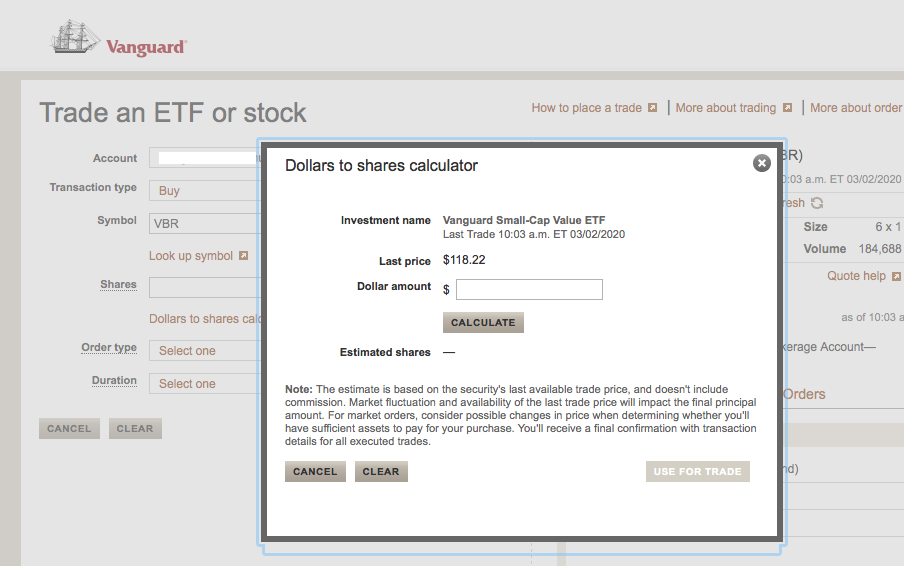

Sale complete. Now I’ve realized a $5,377.72 loss.

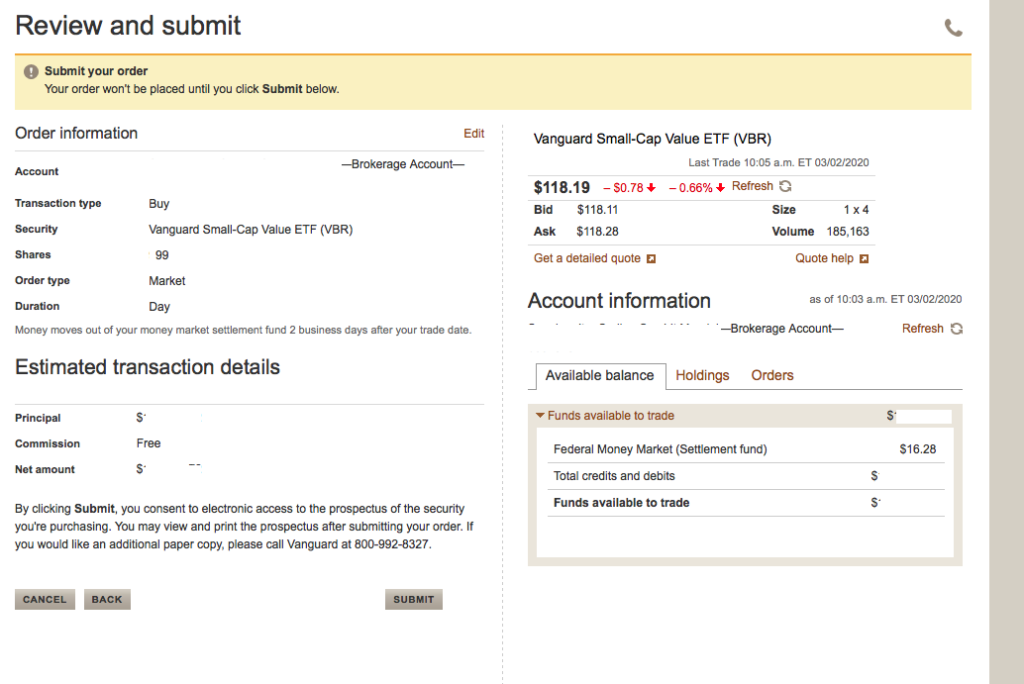

Now comes the TLH part. I will buy a different small-cap value ETF. My default is VBR. I used to have VBR in my Brokerage account but went on a third-degree TLH spree last year and ended up with VIOV.

I use the Dollars to Share Calculator to tell me how many shares of VBR I can purchase with the proceeds of the VIOV sale.

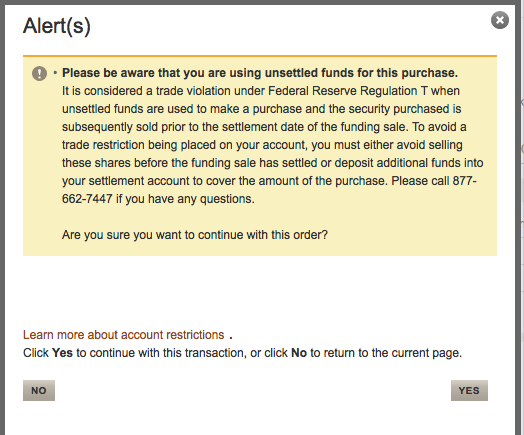

You will get an Alert that looks like this since you’ve just sold that other ETF and the funds from it have not settled into your account yet. Just remember this point in case the market drops further and you wish to TLH again- you can’t sell the VBR in the following 48-72hrs it usually takes.

Once I hit Yes, it takes me to a Review and Submit Screen to complete the purchase. Hit Submit to get to finish line.

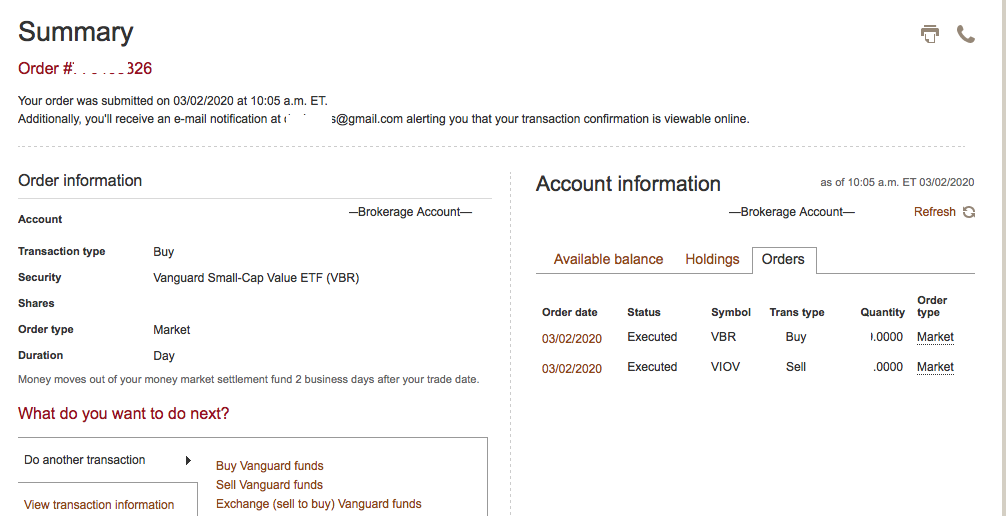

When all is said and done, you get to the Summary screen- which tells you what and how you bought and sold. You do get an email notification, too- so, save some trees.

Well, almost.

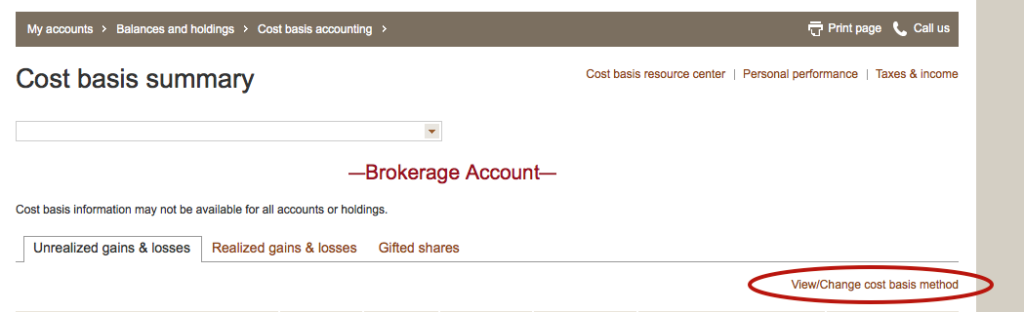

I just quickly go over to the View/Change Cost Basis Method to make sure all of my ETFs are set to Spec ID. Vanguard’s default options is “Average Cost” for Mutual funds and “First in, First out” for individual stocks.

This wasn’t so bad, was it? And $1200 off my tax bill for this year and some more carried over next year. All without breaking a sweat.

Downsides to Tax Loss Harvesting?

- Another thing to do. Hard, especially for doctors busy doctoring, since the market makes all its swingin’ moves during regular business hours.

- Rules to remember. Though there are many and they are simple to follow

- Adds complexity to your portfolio. I have a bunch of ETFs in my Brokerage account, thanks to TLH.

I have both VTI and VOO for Total U.S. Stock Market.

For Total International Stock Market, it’s even worse. I have IXUS (iShares Total International ETF) as well as a combination of Developed Markets (Vanguard FTSE Developed Market ETF: VEA) and Emerging markets (Vanguard FTSE Emerging Market ETF: VWO). All thanks to prior TLH.

I am okay with it, it doesn’t bother me. But some people may feel differently.

- This also reminds me that the replacement ETF must be something you are willing to hold for a while. Because you do not know if or when the next TLH opportunity will present itself.

- The replacement ETF may have a higher expense ratio than your preferred ETF.

- The replacement ETF may not be the exact asset class you desire. For example, VOO is an S&P 500 ETF- not a true Total Stock Market Index. And VIOV is not as Value-y as VBR (if a value tilt is what you are looking for). But for the most part, these differences are small and more theoretical.

- If you held the fund for less than 60 days prior to TLH and received dividends from it, it will not be regarded as Qualified Dividends. Qualified dividends are taxed at capital gains rates while non-qulified dividends are taxed as ordinary income. This increase in tax burden may negate some or all of the benefit of TLH.

Hope this help and helps you take that first step.

Further Reading

- Tax Loss Harvesting– Bogleheads

- A Step by Step guide to Tax Loss Harvesting by White Coat Investor

- Tax Loss Harvesting with Vanguard by Physician on Fire